The Accounting Equation Explained

Understanding the Foundation of Financial Accounting Year 10 Business Studies

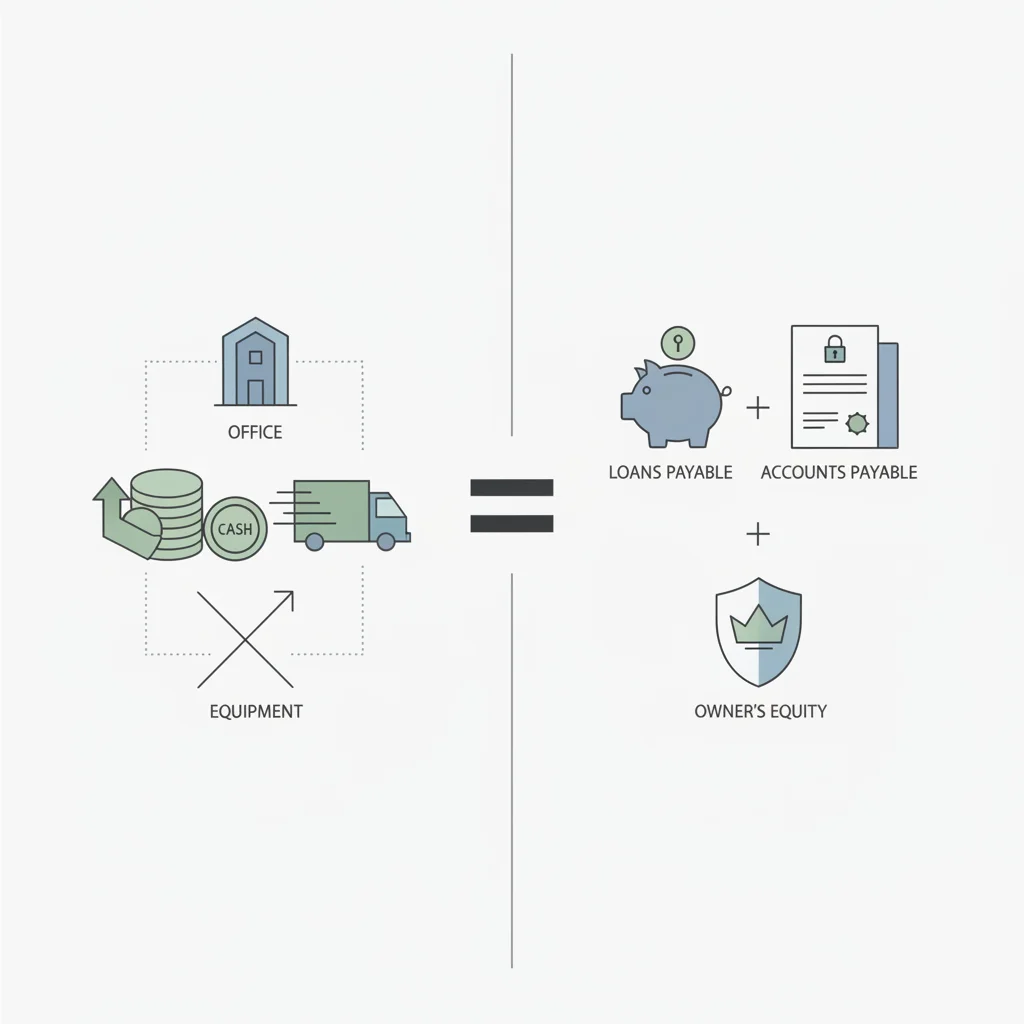

What is the Accounting Equation?

Assets = Liabilities + Owner's Equity The fundamental principle of accounting Every transaction must balance Foundation for all financial statements

Understanding Assets

Resources owned by the business Examples: Cash, inventory, equipment, buildings Current assets vs. non-current assets Provide future economic benefits

Understanding Liabilities

Debts and obligations of the business Money owed to others Examples: Bank loans, accounts payable, mortgages Must be paid in the future

Understanding Owner's Equity

Owner's claim on business assets Initial investment plus retained profits Also called 'Net Worth' or 'Capital' What remains after paying all debts

The Equation in Action

{"left":"A business has $50,000 in assets\nIt owes $20,000 in loans","right":"Owner's equity = $30,000\nCheck: $50,000 = $20,000 + $30,000"}

Practice Problem

Sarah's Bakery has: Equipment worth $15,000 Cash of $5,000 Bank loan of $8,000 Calculate Owner's Equity

Discussion Question

If a business buys equipment for $10,000 cash: How does this affect the accounting equation? Do assets increase or decrease? Does the equation stay balanced?

Transaction Effects on the Equation

Key Takeaway

The accounting equation is the foundation of all financial record-keeping. Every business transaction must maintain the balance: Assets = Liabilities + Owner's Equity